In an ever-changing economic climate, mortgage rates are subject to fluctuations caused by numerous factors. However, one element remains a steadfast predictor of mortgage interest rates: credit scores. Despite market volatility, credit scores continue to be a vital factor in the mortgage approval process. This article delves into how credit scores influence mortgage rates, offering insights into generational credit score trends among Gen Z, millennials, Gen X, and baby boomers.

The Significance of Credit Scores in Mortgage Rates

Lenders heavily rely on credit scores to assess the risk associated with potential borrowers. Today, the connection between credit scores and mortgage interest rates is more pronounced than ever. Higher credit scores suggest lower lending risks, which translates into more favorable interest rates for borrowers. This can result in significant savings over the life of a mortgage.

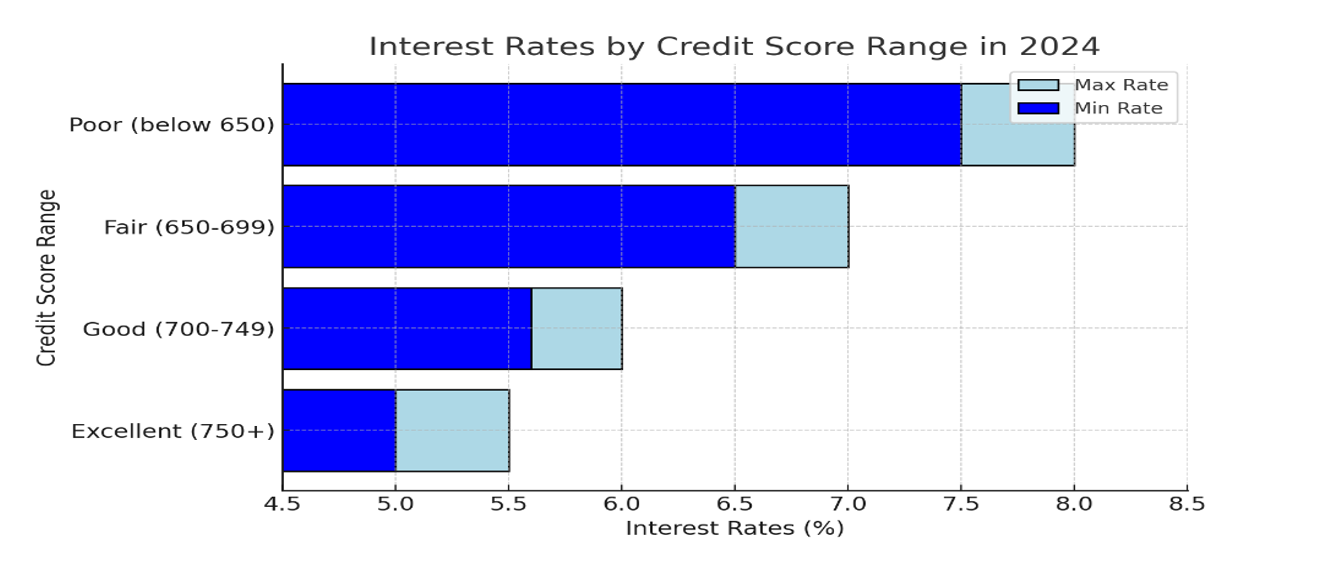

The mortgage industry frequently uses the FICO credit scoring model, ranging from 300 to 850. Here’s how different credit score brackets affect average mortgage rates in 2024:

- Excellent (750+): Borrowers with excellent scores enjoy rates between 5.0% and 5.5%.

- Good (700-749): Rates for this group range from 5.6% to 6.0%.

- Fair (650-699): Interest rates for fair credit scores range between 6.5% and 7.0%.

- Poor (below 650): Rates start at 7.5% for poor scores, with some lenders requiring extra points upfront.

These variations in rates can significantly impact the total cost of a mortgage. For example, a borrower with a 750+ score on a $300,000, 30-year fixed mortgage at 5.0% would pay approximately $1,610 monthly. Conversely, a borrower with a 650 score at 7.0% would pay around $1,995 per month, totaling nearly $138,000 more over the loan’s duration.

Credit Score Trends by Generation in 2024:

According to VantageScore CreditGauge data, generational differences in financial habits, credit access, and economic conditions have led to diverse credit score trends. Let’s explore these trends:

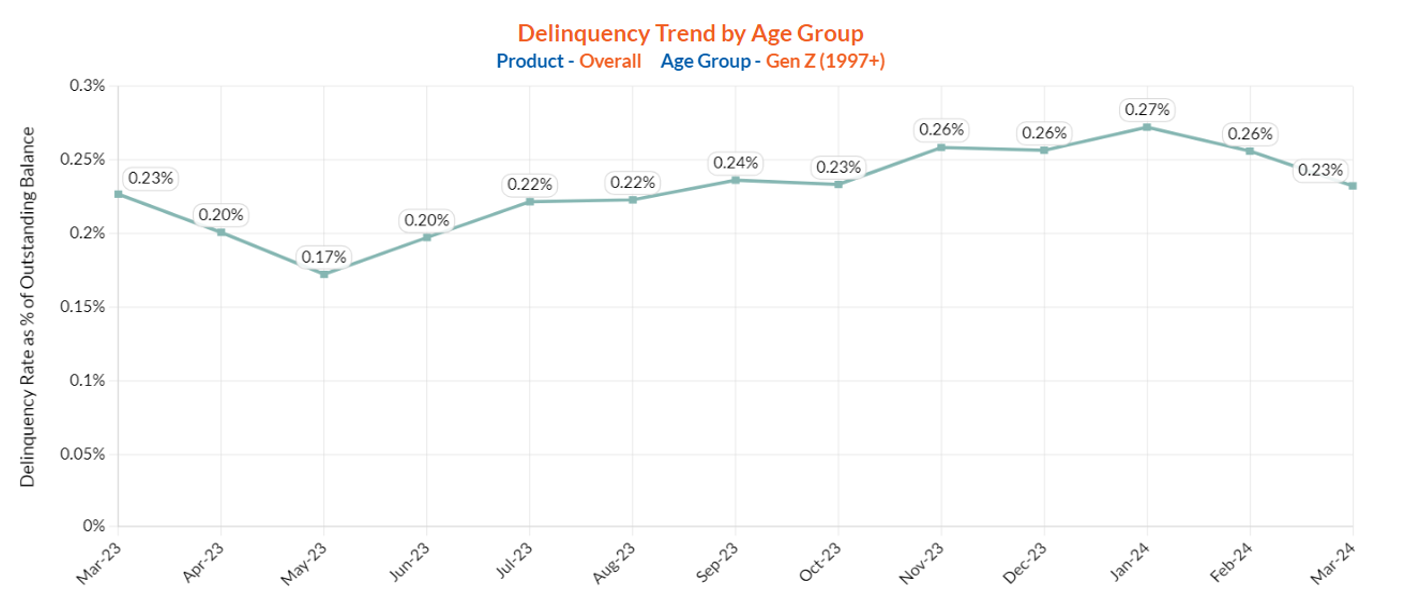

- Gen Z (Born 1997-2012): As Gen Z enters the housing market, their average credit score hovers around 679. A 15% increase in the past two years, driven by financial literacy initiatives and digital resources, has been observed. However, short credit histories often hinder their ability to secure the best mortgage rates.

Here’s a line chart depicting the delinquency rate trend for Gen Z from March 2023 to March 2024, which shows this as a percentage of the outstanding balance.

- Millennials (Born 1981-1996): With an average credit score of 700, millennials are the largest cohort of homebuyers. Many have improved their scores by reducing debt and achieving financial stability, though high student loan debt remains a challenge.

- Gen X (Born 1965-1980): Averaging a credit score of 721, Gen X generally boasts stronger credit profiles due to extensive credit experience. However, some still rebuild from financial setbacks during the 2008 housing crisis.

- Baby Boomers (Born 1946-1964): Leading with an average credit score of 734, baby boomers benefit from long-established credit histories and lower debt levels. These factors, coupled with substantial home equity, afford them favorable rates as they transition into retirement.

Here’s a bar chart illustrates the range of mortgage interest rates in 2024 across four credit score categories: Poor (below 650), Fair (650-699), Good (700-749), and Excellent (750+).

What Improving Credit Scores Mean for Lenders

The upward trend in credit scores across generations presents significant opportunities for lenders. As borrowers improve their credit profiles, lenders face reduced risks, which can lead to a more stable lending environment. This improved risk assessment not only enhances the lenders’ ability to offer competitive rates but also increases the potential for higher loan approval rates, fostering customer satisfaction and loyalty.

Moreover, as credit scores rise, lenders can diversify their product offerings, tailoring mortgage solutions to meet the varying needs of a more creditworthy clientele. This diversification can boost profitability by attracting a broader customer base, enabling lenders to capitalize on emerging market segments that were previously underserved due to credit constraints.

The Importance of Understanding Client Credit Histories

For lenders, a deep understanding of client credit histories is essential in making informed lending decisions. A comprehensive view of a borrower’s financial behavior allows lenders to better assess risk levels and tailor products that meet the specific needs of their clients. By leveraging both first-party and third-party data, lenders gain a holistic picture of borrower profiles, enhancing the accuracy of credit assessments and decision-making processes.

Investing in consumer credit data is crucial for lenders aiming to remain competitive in a rapidly evolving financial landscape. Access to detailed and up-to-date credit information, coupled with advanced analytics, enables lenders to identify trends and anticipate borrower needs, ultimately improving the precision of credit offerings and fostering stronger customer relationships.

Harnessing DataVue for Enhanced Consumer Insights

DataVue offers cutting-edge solutions that empower lenders with robust insights into consumer credit data. By integrating machine learning models that utilize both consumer credit and alternative data, DataVue provides lenders with a comprehensive toolset for evaluating borrower potential. This approach ensures that lenders are equipped with the most accurate and relevant information, enabling them to make confident lending decisions.

The Precision Pulse feature within DataVue takes lender insights a step further by delivering daily alerts on in-market borrowers. This proactive approach allows lenders to swiftly respond to emerging opportunities, ensuring they can engage potential clients at optimal moments. By leveraging DataVue’s advanced analytics and real-time data capabilities, lenders can maintain a competitive edge in the dynamic mortgage market.